- Americans are steadily falling deeper into credit card debt.

- There are some tried-and-true payoff strategies that can help, experts say.

- Here are the best ways to jump-start debt repayment.

Credit cards are the Achilles' heel for most people.

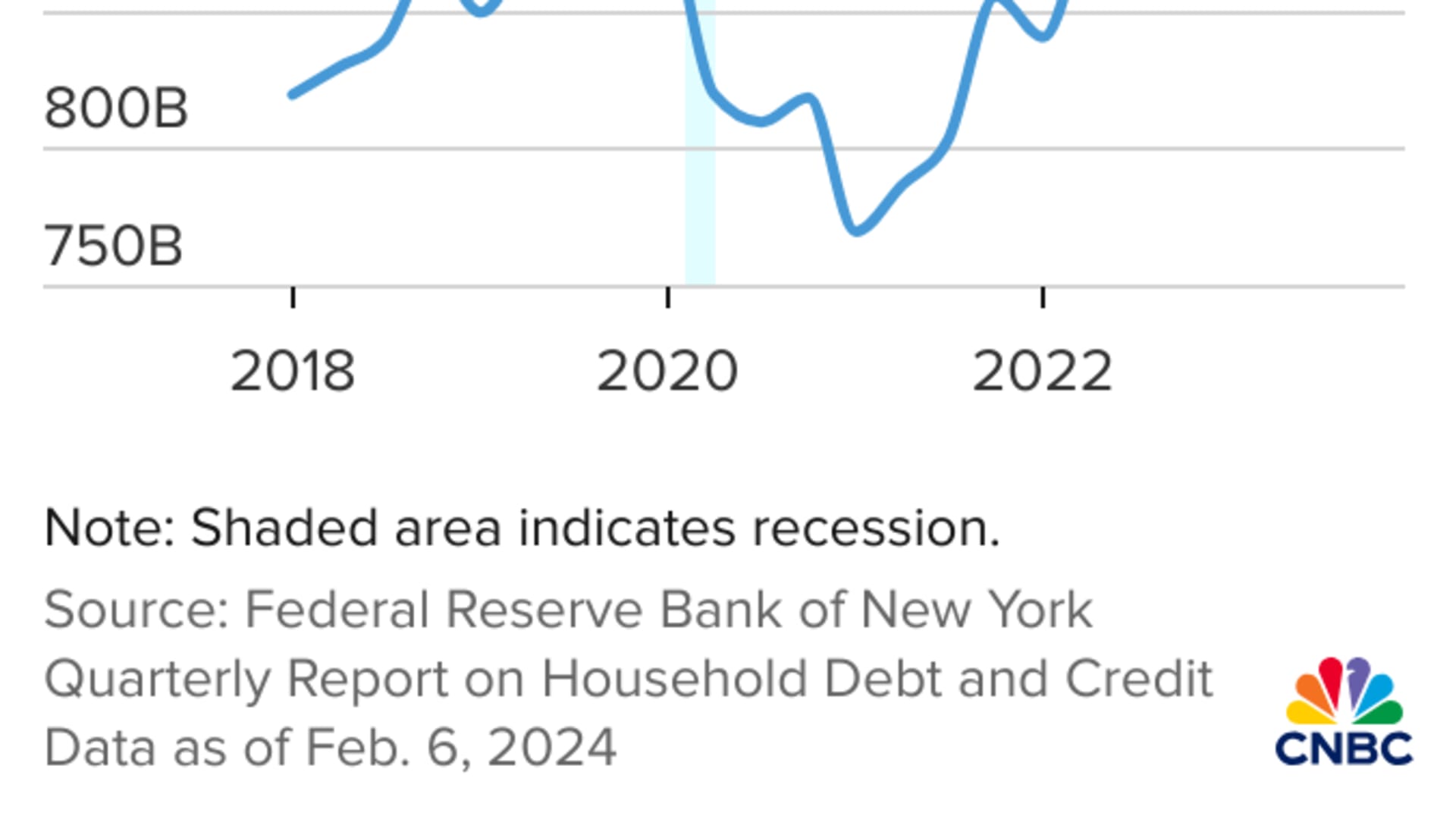

Collectively, Americans now owe $1.13 trillion on their cards and the average balance per consumer is up to $6,360, both historic highs.

Not only are more cardholders carrying debt from month to month but they are also increasingly falling behind on payments, recent reports show.

"Even though dealing with $1 trillion in credit card debt can be overwhelming, the reality is that this figure is expected to ascend," said Tomas Philipson, a professor of public policy studies at the University of Chicago and former acting chair of the White House Council of Economic Advisers.

Money Report

"Americans are still contending with lingering inflation and the ongoing rise in interest rates, which forces them to depend more heavily on credit cards," Philipson said.

More from Personal Finance:

Average credit card balances jump 10% to a record $6,360

Credit card debt hits a 'staggering' $1.13 trillion

Americans can't pay an unexpected $1,000 expense

Already, credit cards are one of the most expensive ways to borrow money. The average credit card charges a record high 20.74%, according to Bankrate.

But there are proven pay-off strategies that work, experts also say. Here is their best advice for tackling that high-interest debt once and for all, including one analyst's "favorite tip."

Here are two ways to jump-start debt repayment

1. Try a 0% balance transfer credit card

"My favorite tip is to sign up for a 0% balance transfer credit card," said Ted Rossman, senior industry analyst at Bankrate.

Cards offering 12, 15 or even 21 months with no interest on transferred balances are out there, he added, and "these allow you to consolidate your high-cost debt onto a new card that won't charge interest for up to 21 months, in some cases."

Those offers are "just about the best tool you have against credit card debt," added Matt Schulz, chief credit analyst at LendingTree.

To make the most of a balance transfer, aggressively pay down the balance during the introductory period. Otherwise, the remaining balance will have a new annual percentage rate applied to it, which is about 24.6%, on average, in line with the rates for new credit, according to Schulz.

Further, there can be limits on how much you can transfer, as well as fees attached.

Most cards have a one-time balance transfer fee, which is usually around 3% of the tab, but "it's becoming more common to find cards charging 4% or 5% as a balance transfer fee, which is something people should be aware of," Schulz said.

Borrowers may also be able to refinance into a lower-interest personal loan. Those rates have climbed recently, as well, but at just under 12%, on average, are still well below the current credit card average.

Otherwise, ask your card issuer for a lower annual percentage rate. In fact, 76% of people who asked for a lower interest rate on their credit card in the past year got one, according to a LendingTree report.

2. Pick a repayment strategy

There are two ways you could approach repayment: prioritize the highest-interest debt or pay off your debt from smallest to largest balance. Those strategies are known as the avalanche or snowball method, respectively. Using either can help consumers pay off debt as much as 100 months sooner, according to a separate analysis by LendingTree.

The avalanche method has you list your debts from highest to lowest by interest rate. That way, you start paying off the debts that rack up the most in interest first. The snowball method prioritizes your smallest debts first, regardless of interest rate, to help gain momentum as the debts are paid off.

With either strategy, you'll make the minimum payments each month on all your debts and put any extra cash toward accelerating repayment on one debt of your choice.

"If I were to pick one for myself, I would probably go with avalanche because the math works out the best," Schulz said, "but ultimately, it really doesn't matter — it's about picking the one that's going to be the most motivating to you and the one you are most likely stick with."