Op-Ed: Black Women Must Make Their Own Magic With Their Finances

- Millennials' average net worth more than doubled during the pandemic, jumping to $127,793 during the first quarter of 2022.

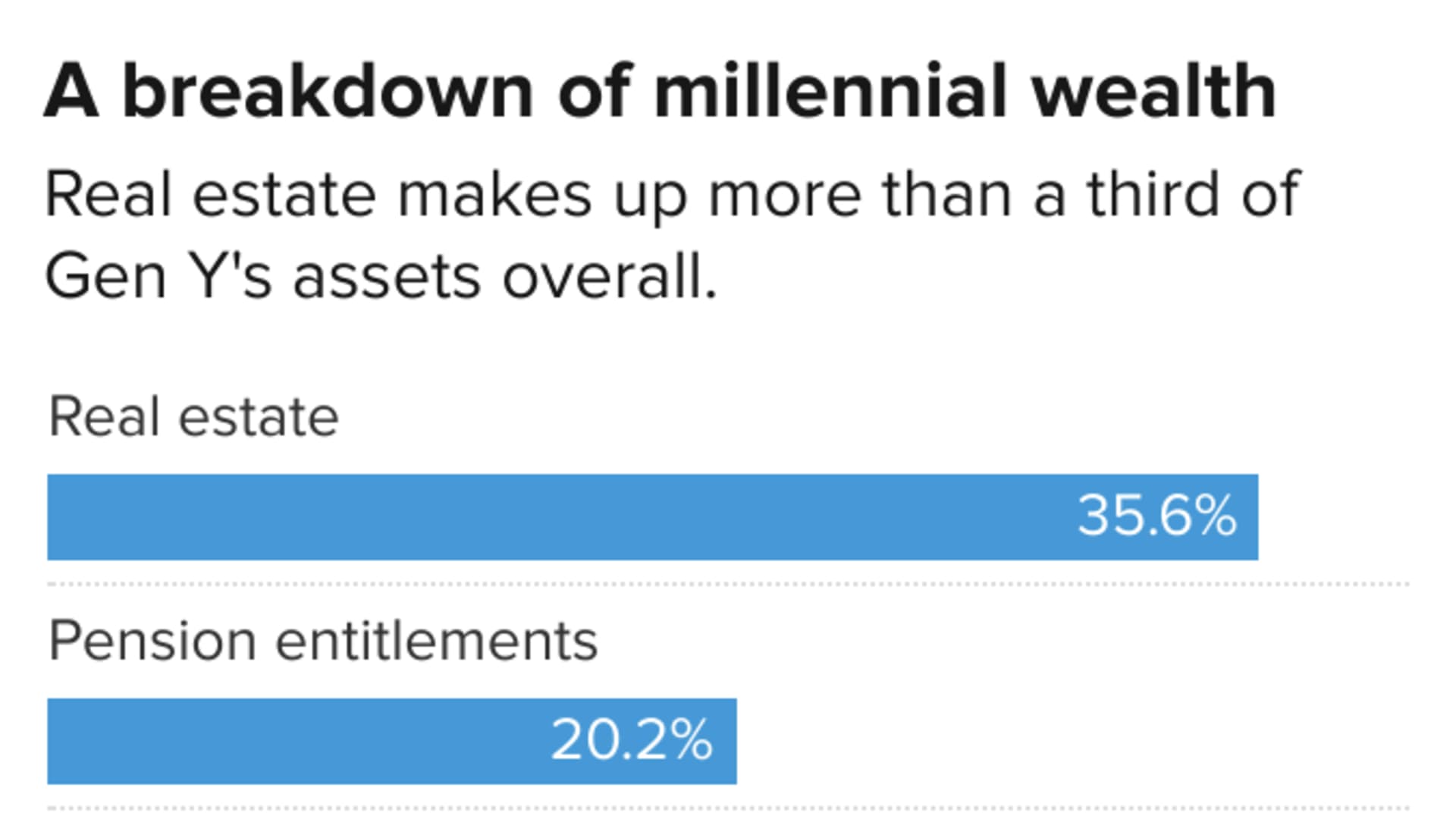

- The largest percentage of millennial assets is real estate, making up more than one-third of their wealth.

- Experts suggest focusing on other assets, such as building retirement plans and other long-term investments.

Covid-19 relief and record-low interest rates boosted many Americans' finances during the pandemic. That has been especially true for millennials, who have on average built significant wealth.

Millennials, born between 1981 and 1996, have more than doubled their total net worth, reaching $9.38 trillion in the first quarter of 2022, up from $4.55 trillion two years prior, according to a MagnifyMoney report.

And millennials' average net worth — defined as total assets minus total liabilities — also increased twofold during the same period, jumping to $127,793 from $62,758, the report found.

More from Personal Finance:

Nearly half of all Americans fall deeper in debt as inflation boosts costs

1 in 5 Americans dodging credit card statements as interest rates spike

Gen Z is stashing away 14% of income for retirement, study shows

However, the report finds the average millennial net worth still lags behind older generations, with Gen Xers and baby boomers reaching an average of $647,619 and $1,021,264, respectively.

Real estate more than a third of millennial wealth

With soaring home values over the past couple of years, it's not surprising that real estate, including primary homes and other property, is more than one-third of millennials' total assets.

Money Report

The median U.S. home sales price was $329,000 during the first quarter of 2020, and the number jumped to nearly $429,000 two years later, according to Federal Reserve data.

However, millennials who recently bought homes may have significant debt, the report found. Nearly 63% of millennial debt is home mortgages, followed by almost 36% in consumer credit.

"I would encourage millennials to focus more on their cash flow than net worth in this stage of their careers," said certified financial planner DJ Hunt, senior financial advisor with Moisand Fitzgerald Tamayo in Melbourne, Florida.

He said millennials may be "losing financial ground in the long run" if monthly mortgage payments prevent them from fully funding their retirement accounts.

Of course, the definition of a fully funded retirement account varies by individual, Hunt said.

While older millennials in their early 40s should aim to max out 401(k) contributions at $20,500 in 2022, younger workers should deposit enough to receive their company match, striving for up to 15% of gross income, he said.

Diversification is 'name of the game'

Although owning and living in your home serves an important purpose, diversification is "the name of the game," especially for younger investors with more time to build assets, said Eric Roberge, a CFP and CEO of Beyond Your Hammock in Boston.

If most of your wealth is home equity, it may be wise to focus on building retirement plans or a brokerage account, he said, suggesting 20% to 25% of gross income annually for long-term investments.

"For many people, a diversified portfolio will likely provide higher returns in the long-term," he said.

Applying for a home equity line of credit

If you're sitting on wealth in your home, it may be worthwhile to apply for a home equity line of credit, or HELOC, allowing you to borrow from a pool of money over time, if needed.

"It is always a good idea to have a HELOC in place if you have substantial equity in your home," said Ted Haley, a CFP, president and CEO of Advanced Wealth Management in Portland, Oregon.

HELOCs are typically inexpensive to set up, with lower interest rates than credit cards, and there's no added cost until you use it. While higher interest rates may impact how much and when to borrow, it's still a "good idea" to have one, he said.