To Make Your Financial New Year’s Resolutions Stick, Here’s What You Need to Do

People have the best of intentions.

At the start of a new year, millions make resolutions — goals they want to reach throughout the upcoming months. Getting a handle on money issues is usually near the top of many such lists.

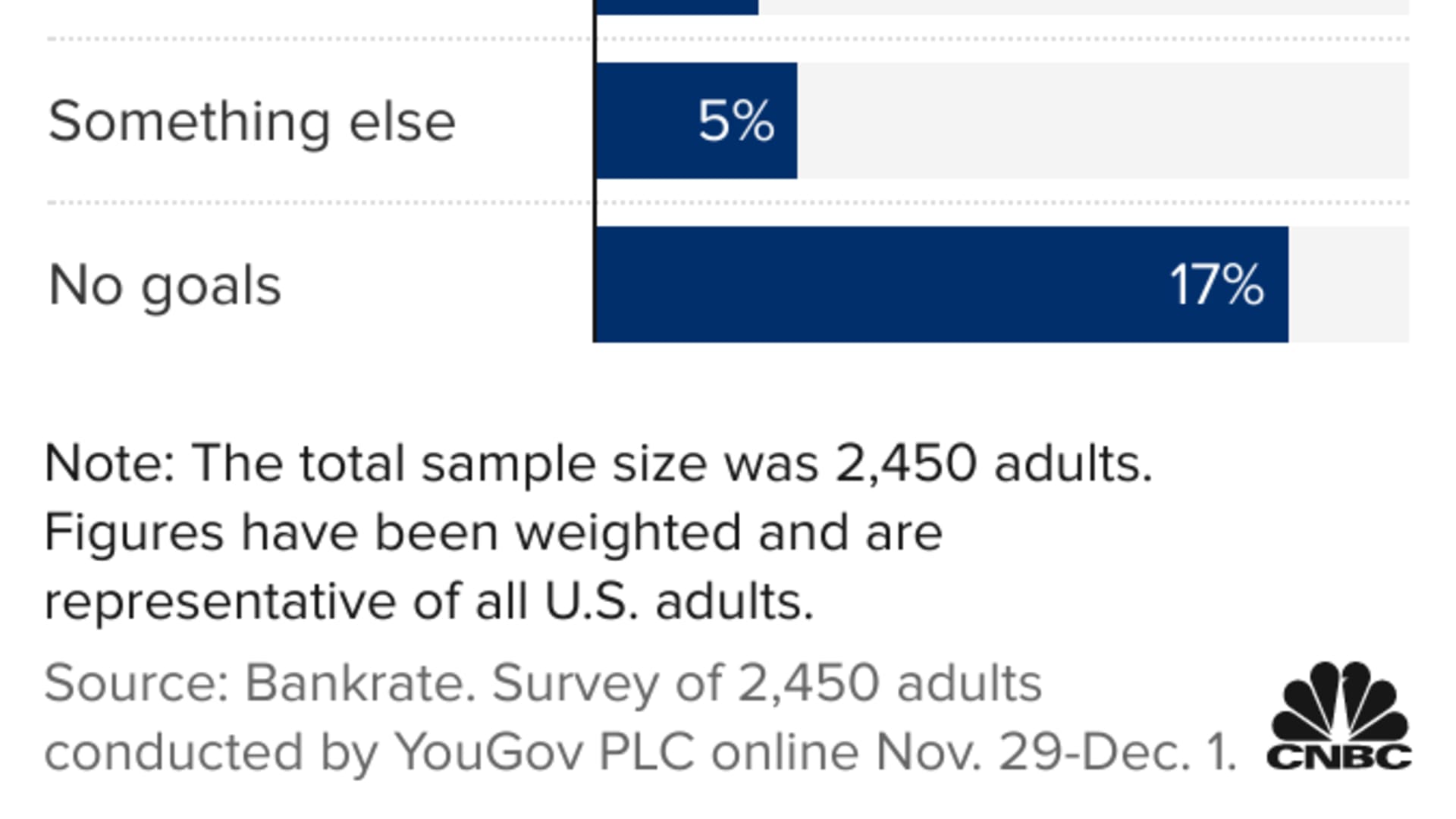

The most financial popular goals are paying down debt, saving for emergencies, budgeting better and saving more for retirement, a Bankrate poll found.

The problem is that most people fail to keep their New Year's resolutions.

"It is so easy to get off track," said financial expert Steve Siebold, author of "How Money Works."

"Everyone wants to make more money, save more money, invest more," he added. "But when it comes down to it, we tend to react emotionally instead of logically and that is the downfall."

There is some good news, however. Those who made resolutions at the start of 2021 are more optimistic about the future than those who didn't, a survey from Fidelity Investments found.

Money Report

Eighty-one percent of respondents who made resolutions said they will be better off financially in 2022, compared to 58% of those who didn't make any promises, according to the survey, conducted Oct. 18-24, 2021, among 3,031 adults 18 or older, by ENGINE Insights.

Here's what you can do to make sure you stick to your resolutions — and what to do if you fall off track.

Find your motivation

The first thing to do is tap into your emotions, before you even think about numbers, said Siebold.

"While it's important to focus on how you are going to do it, the very first step is to focus on 'why' you are doing it," he said.

"Without a driving motivator or reason, the 'how' doesn't matter."

For example, it may mean thinking about relocating to someplace warm or moving closer to grandchildren when saving for retirement.

Start small

It's easy to get overwhelmed, especially if you are trying something new.

"Start with small, manageable goals," said Teresa Jacobsen, managing director at UBS Private Wealth Management in Stamford, Connecticut.

That can work with contributing to your retirement savings, for instance. Just putting aside a little bit can start the habit and you can increase it when you are able.

The same goes if you have a laundry list of financial goals. Remember, you don't have to do it all at once, said Kelly LaVigne, vice president of consumer insights at Allianz Life.

"I might not go the whole way. I might not get in touch with a financial advisor this year," he said. "I might not even make a retirement plan, but let me try to track my expenses for two months and see just what I spend."

Whatever your plan, be sure to write it down.

Pay yourself first

If you want to start an emergency fund or save more for retirement, follow the old adage "pay yourself first." Jacobsen said.

You can set up automatic contributions from your paycheck into your 401(k), for instance. There are also many financial services firms that will transfer money from your paycheck or checking account into a separate savings account, she said.

Stop holding yourself back

Just because you may have failed in the past doesn't mean you will again.

Think about what you can do differently so that you can stick to your goals this time, Siebold said. It may be as simple as giving yourself some sort of reward when you hit a goal.

Have accountability

It will help if you tell people about your specific resolutions, Siebold believes.

You don't have to give them specific figures but ask them to hold you accountable.

Create highly defined goals

Be very specific about what it is you want to accomplish, even down to a certain number you want to save or amount of debt you want to pay off, Siebold said.

More from Invest in You:

26% of Americans expect their finances to be worse in 2022. Here's why

More than 60% of voters support some student loan debt forgiveness

January is one of the best times of the year to look for a job. What to do

It even helps to set a date and backtrack from there to determine how to make it work. The shorter the timeline, the more successful most people seem to be, he said. He suggests setting small goals for every 30 days or quarter so you get the psychological reward each time you hit a goal.

Give yourself a break

The Covid-19 pandemic has been a stressful time, so don't be too hard on yourself.

In fact, treat yourself occasionally, as long as you don't go overboard, LaVigne said.

"You don't want to totally cut off all the fun stuff, because that's what life is all about," he said. "But you want to make sure you can live that life for the next for the 25 or 30 years."

If you fall off track in achieving your goals, don't get upset. Just pick yourself back up and try again.

"Keep at it," said UBS's Jacobsen said.

"Remember what motivates you and why you are doing this."

SIGN UP: Money 101 is an 8-week learning course to financial freedom, delivered weekly to your inbox.

CHECK OUT: I quit my 9-to-5 to run my side hustle once I could pay myself $4,000 a month: Here’s my best advice with Acorns+CNBC

Disclosure: NBCUniversal and Comcast Ventures are investors in Acorns.